Definition of portfolio management

Portfolio management is the discipline of selecting, monitoring and adjusting, as needed, a portfolio of investments whose combination aims to achieve an optimal balance between return and risk.

Building your portfolio: the importance of diversification

An investment portfolio aims to generate returns on your wealth while taking into account the level of risk you are willing to accept. Some financial instruments offer higher return potential but are more volatile and therefore riskier. Others prioritise stability, generally at the expense of lower returns.

A portfolio can be composed of various asset types. For the sake of simplicity, we will focus here on three main asset classes:

- Cash offers little or no return, but provides flexibility to seize investment opportunities or make portfolio adjustments when needed;

- Bonds are among the least risky asset classes and generally offer lower but more predictable returns;

- Equities are subject to higher volatility and larger fluctuations, but in return provide greater potential for long-term performance.

A balanced investment portfolio is built on an appropriate allocation between equities, bonds and cash. At Piguet Galland, as with other financial institutions, this allocation can be enhanced with additional instruments such as real estate funds, alternative investments or commodities, particularly precious metals. This approach aims to take advantage of the performance potential of certain assets while limiting the portfolio’s overall risk through more stable and predictable investments.

It is also important to diversify investments within each asset class. In the case of equities, for example, this means spreading allocations across large-, mid- and small-cap companies, as well as across different sectors. Such diversification helps reduce asset-specific risks and strengthens the portfolio’s overall resilience in response to market developments.

Some examples of standard portfolios

To give you a clearer idea of the different ways you can build an investment portfolio, here are three standard examples: a conservative portfolio, a dynamic portfolio and a balanced portfolio.

- Conservative portfolio: 60% bonds, 35% equities, 5% cash

This type of portfolio prioritises capital preservation by investing mainly in low‑risk, fixed‑income instruments. Its primary objective is to maintain the value of the portfolio over time. A limited allocation to equities is nevertheless included to benefit from their return potential and help offset the effects of inflation. - Dynamic portfolio: 25% bonds, 70% equities, 5% cash

In contrast to a conservative strategy, this portfolio places a strong emphasis on equities in order to take advantage of their long‑term growth potential. Bonds play a diversification role and help mitigate part of the risk. In return, this allocation results in higher volatility and is suitable for investors willing to accept significant fluctuations in exchange for higher return prospects. - Balanced portfolio: 40% bonds, 55% equities, 5% cash

This type of portfolio offers a balanced approach between conservative and more aggressive strategies. Its goal is to benefit from the growth potential of equities while maintaining a substantial allocation to bonds to limit risk. Expected returns are lower than those of an aggressive portfolio, but risk is more closely controlled, making it well suited to investors seeking a compromise between performance and stability.

Monitoring and adjusting your portfolio

It is very likely that you will need to make adjustments to your investment portfolio depending on the performance of financial markets. For example, you may decide to buy or sell a given security or to adjust your asset allocation strategy. That's why each of these portfolios includes a cash component.

At times, it may also be necessary to make adjustments in order to remain aligned with your initial strategy. For example, if the value of your equities increases more than that of your bonds, their weight within the portfolio may rise as a percentage. To restore the desired allocation, you would then need to sell some equities or purchase additional bonds. This process is known as portfolio rebalancing.

A tailored solution based on your profile

The portfolios presented above are for illustrative purposes only and can be adjusted to reflect your personal preferences. There is no universally ideal portfolio, only the one that best matches your investor profile and individual needs. Your investment strategy may vary significantly depending on a range of factors, such as your age, financial situation, life plans, personal interests and risk tolerance.

If you are a young investor at the beginning of your career, you may opt for a more agressive strategy with a long investment horizon, giving you greater potential to achieve your goals. Conversely, if you are approaching retirement and wish to consolidate your assets, a more conservative approach is generally more appropriate.

The composition of your portfolio may also be influenced by your personal interests or by the amount of time you are willing to devote to managing your investments. For example, you may choose to focus on specific geographic regions or sectors you consider particularly promising. Depending on your preferences, you may select individual investments based on your own analysis and convictions, or opt for investment funds to simplify the selection and diversification process.

You can also choose to rely on professional expertise, either through a discretionary mandate or an advisory mandate, to benefit from tailored guidance and support.

Piguet Galland notably offers a dedicated Distribution management mandate, designed to meet regular liquidity needs, such as supplementing income from professional activity or retirement pensions. This solution is particularly suited to investors seeking to preserve their standard of living. Based on the invested capital, the distribution strategy aims to provide a stable and predictable income stream. It relies on globally diversified sources of income, such as coupons, dividends and option premiums, and may offer certain tax advantages for Swiss residents. This diversified, multi‑asset portfolio is composed of financial instruments selected not only for their income‑generating potential, but also for their resilience, thereby contributing to capital preservation.

There is no single way to invest, only solutions tailored to each investor profile. Our teams of experts are at your disposal to support you in your first steps and help you structure both your portfolio and your investment strategy.

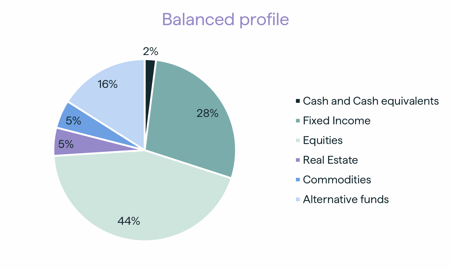

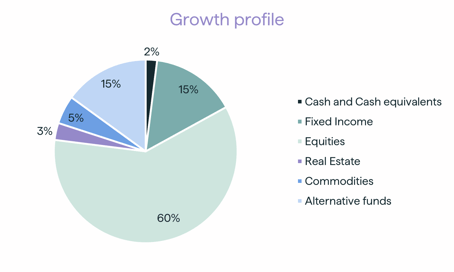

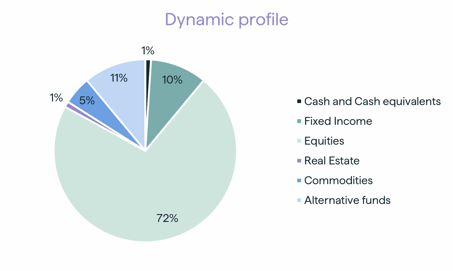

Allocations of three profiles in CHF