Episode 1/6

![]()

Retirement involves navigating multiple sophisticated dimensions, from state and occupational pension systems to insurance, tax matters, property, and investment management. Each person’s circumstances are distinct, defined by their background and objectives. Through our 360 series, we answer your key questions and deliver personalised insights to support your preparation for this essential life milestone.

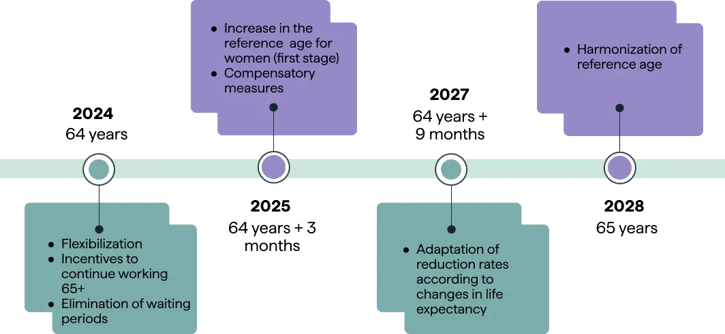

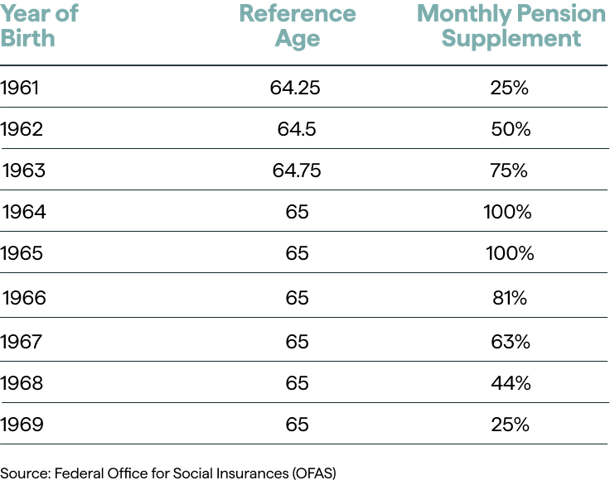

As a result, women born between 1961 and 1969 will receive lifelong pension supplements as a compensatory measure. The amount of these supplements will vary depending on the year of birth.

Changes may occur over time, but with proper preparation, you will be able to manage them and minimise their impact on your retirement plan. It is essential to carefully determine the date of your retirement, whether you are considering early retirement or planning to extend your career. Establish a budget that allows you to live comfortably and pursue your goals, while ensuring that your income will be sufficient to cover your expenses.

Don’t wait: open your Excel spreadsheet and list your monthly and annual expenses. This will give you a clear sense of your financial needs in retirement. Keep in mind that some work‑related costs, such as commuting and meal expenses, will disappear, and certain insurance premiums will decrease slightly. However, supplementary health insurance becomes more expensive as you age.

In the upcoming episodes, we will take a closer look at the various dimensions of retirement, including the state pension system, the choice between an annuity or a lump sum, tax implications, early retirement, mortgages, and expatriation.

For now, let’s begin by focusing on the key dates you need to prepare for your dolce vita.

Financial strategies by life stage

Ages 30 to 45: Build strong wealth early

Whether you are 30 or 45, it is important to establish a solid savings strategy to ensure long‑term financial security.

For example, in 2025, Caroline, age 35, living in Lausanne with a taxable annual income of CHF 70,000, can contribute up to CHF 7,258 to her Pillar 3a account. If she chooses to contribute only CHF 4,000, she will benefit from a tax saving of CHF 938 for the 2025 tax year. By continuing to contribute CHF 4,000 each year until age 65, she will have accumulated CHF 100,000 in savings and earned CHF 42,615 in interest at a rate of 2.5%.

Ages 50 to 55: Optimise your retirement strategy

As you approach your fifties, preparing for retirement becomes essential, as you have around fifteen years left to secure your financial position for the years ahead.

-

Refine your occupational pension strategy (Pillar 2)

By requesting the maximum allowable contributions and closing any existing gaps through targeted buy‑ins.

-

Maximise your contributions to existing Pillar 3 accounts

And, if you haven’t already, build a financial safety reserve to cover unexpected expenses.

-

Consider seeking guidance from a wealth management specialist

To gain a holistic view of your financial situation and plan your next steps with confidence.

Five years before retirement: Make key decisions

As you approach the five‑year mark before retirement, this period becomes crucial for making the essential decisions that will ensure a smooth and well‑planned transition into the next stage of your life.

-

Retirement date

Determine your planned retirement date, clarify the payment options with your pension fund (whether you choose an annuity or a lump‑sum withdrawal), and carefully assess all available alternatives.

If you opt for a lump‑sum withdrawal, make sure to submit your decision within the required deadlines and evaluate whether making additional buy‑ins to your occupational pension fund could help optimise your tax situation.

-

Real estate

Decide whether you intend to partially or fully amortise your mortgage, and adjust the maturity accordingly.

You should also define when you wish to withdraw your Pillar 2 and Pillar 3 pension assets. By staggering these withdrawals over several years, you may be able to achieve significant tax savings.

Take stock of your financial situation

Our experts support you at every step to help you make the most suitable decisions for your retirement.